The Micro DAX (Deutscher Aktienindex) Futures gives investors exposure to the 40 largest blue-chip German companies traded on the Frankfurt Stock Exchange. It represents about 80% of the market capitalization of listed stock corporations in Germany.

Top constituents include legacy automakers such as Bayerische Motoren Werke (BMW), Volkswagen, and Mercedes-Benz. Other notable companies that most people know of include Adidas, Siemens, SAP, Infineon, Allianz, and Airbus.

Germany’s historical status as a manufacturing and export powerhouse has given it the world’s 2nd largest trade surplus (exports outweigh imports), just behind China.

Transition to Fiscal Expansion

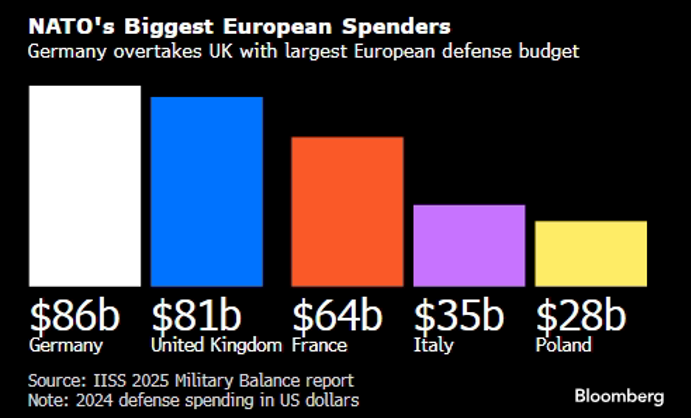

In a historically unprecedented fiscal policy shift, Germany amended its constitution to exempt defence and security outlays from its limits on fiscal spending, while also agreeing to launch a €500 billion infrastructure fund to invest in national priorities such as transportation, energy grids, and housing.

We believe this fiscal shift will remain for some time, with the US likely to pare back its security presence on the European continent, making defence spending all the more important.

Defence spending is expected to exceed 1% of GDP, partially funded by a loosening of the constitutional “debt brake”. This has driven shares of defence company, Rheinmetall AG (+92.43% LTM) towards record highs. German bond yields rose because of expectations of higher debt issuance to fund higher fiscal outlays. The Euro, meanwhile, is at its strongest since 2021.

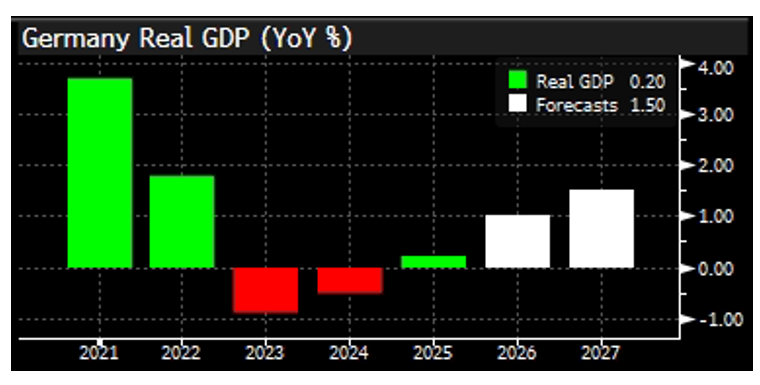

Economic Recovery

The German economy was able to shift from consecutive years of stagnation toward a slow recovery driven by increased public spending. The Bundesbank cited growth in industry and notable strength in construction.

Monetary Policy

The ECB has maintained a supportive backdrop with gradual interest rate cuts to approximately 2%.

Recent reports suggest the ECB President Christine Lagarde could step down before her 8-year term ends in October 2027. Such a decision will likely add volatility to the trajectory for monetary policy.

Tariff Tensions

On February 20, 2026, the US Supreme Court struck down reciprocal tariffs previously imposed by the Trump administration.

This triggered a sharp rally in the export-heavy automotive sector, with Porsche (+1.53%), Mercedes-Benz (+1.08%), and BMW (+0.44%) seeing immediate gains.

Top Performing Sectors LTM (Last Twelve Months)

- Defence: Higher European defence budgets have driven massive gains in Rheinmetall (+92.43%).

- AI Winners: E.ON AG (+64.56% LTM), RWE AG (+84.65% LTM) and Siemens Energy (+181.57% LTM) have capitalised on AI-driven energy demand and digitalisation.

- Siemens reported a record-breaking €146 billion order backlog, a sharp recovery in its wind division, and surging electricity demand fuelled by the global expansion of AI data centres. The Gas Services division saw its highest quarterly order intake ever, booking 102 gas turbines.

- Siemens’ 1Q26 Net Income nearly tripled YoY to €746 million. Free cash flow reached a record €2.9 billion, nearly double the previous year’s result, buoyed by large advance payments from new orders.

Valuations:

The DAX continues to trade at a relative discount to US indices like the S&P 500, with a LTM P/E ratio around 18x for the DAX compared to 25.6x for the S&P 500.

However, the blistering rally has left valuations looking stretched on an absolute basis, at 18 times earnings, the index is trading higher than the 5-year average multiple of 15.5x.

Conclusion

Defence spending and a Russia-Ukraine resolution will be the key drivers for the DAX index. Stretched valuations leave the DAX vulnerable to a short-term drawdown due to geopolitical tensions (e.g., Tariffs). A strengthening Euro is an emerging risk that may weigh on export competitiveness later in 2026.

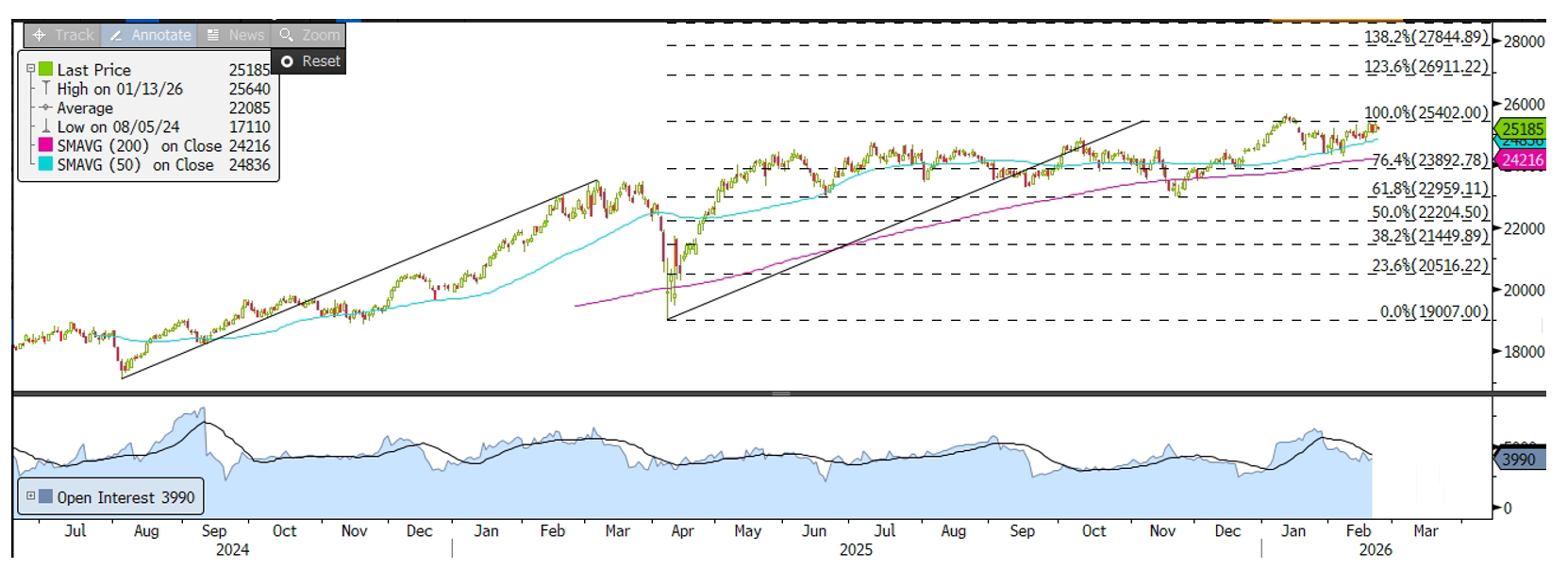

Based on the Micro DAX Future’s daily chart, we expect the contract to hover rangebound between the 100% extension level of 25,402 and 76.4% extension level of 23,892 in the near-term.

If geopolitical tensions continue to escalate and Germany’s economy continues to stagnate, we may see the contract break below the 76.4% extension level to test 23,000, around the 61.8% extension level.

On the other hand, a resolution to the Russia-Ukraine conflict and a continued economic recovery in Germany, accompanied by stable bond yields, could push the contract further upwards, above immediate resistance at 25,400, and towards 27,000 which hovers around the 123.6% extension level.

Take a view on the European Markets with Phillip Nova now!

Trade Micro-DAX® and Micro-EURO STOXX 50® Futures at EUR1.50*. Learn more here.